Want more real estate stories from Lance Lambert? ResiClub in your inbox? Subscribe to ResiClub information sheet.

During the pandemic housing boom, demand for housing rose rapidly amid ultra-low interest rates, stimulus, and the rise of remote work, which increased demand for space and unlocked “WFH arbitrage” as high earners were able to maintain their income from a job in, say, New York or Los Angeles, and buy in, say, Austin or Cape Coral-Fort Myers, Florida. Federal Reserve researchers estimate that “new construction would have had to increase by approximately 300% to absorb the surge in pandemic-era demand.”

Unlike housing demand, housing supply is not as elastic and cannot increase as quickly. As a result, pandemic-era demand depleted the market’s active inventory and overheated home prices, with U.S. home prices rising a staggering 43% between March 2020 and June 2022.

While many commentators view active inventory and months of supply simply as measures of “supply,” ResiClub sees them more as indicators of the balance between supply and demand. Because housing demand is more elastic than housing stock, large swings in active inventory or months of supply are often driven by changes in demand.

For example, during the pandemic housing boom, increased demand caused homes to sell faster, driving down active inventory even as new listings remained stable. Additionally, in recent years, weakening demand has caused a slowdown in sales, causing active inventory to increase even as new listings fell below trend.

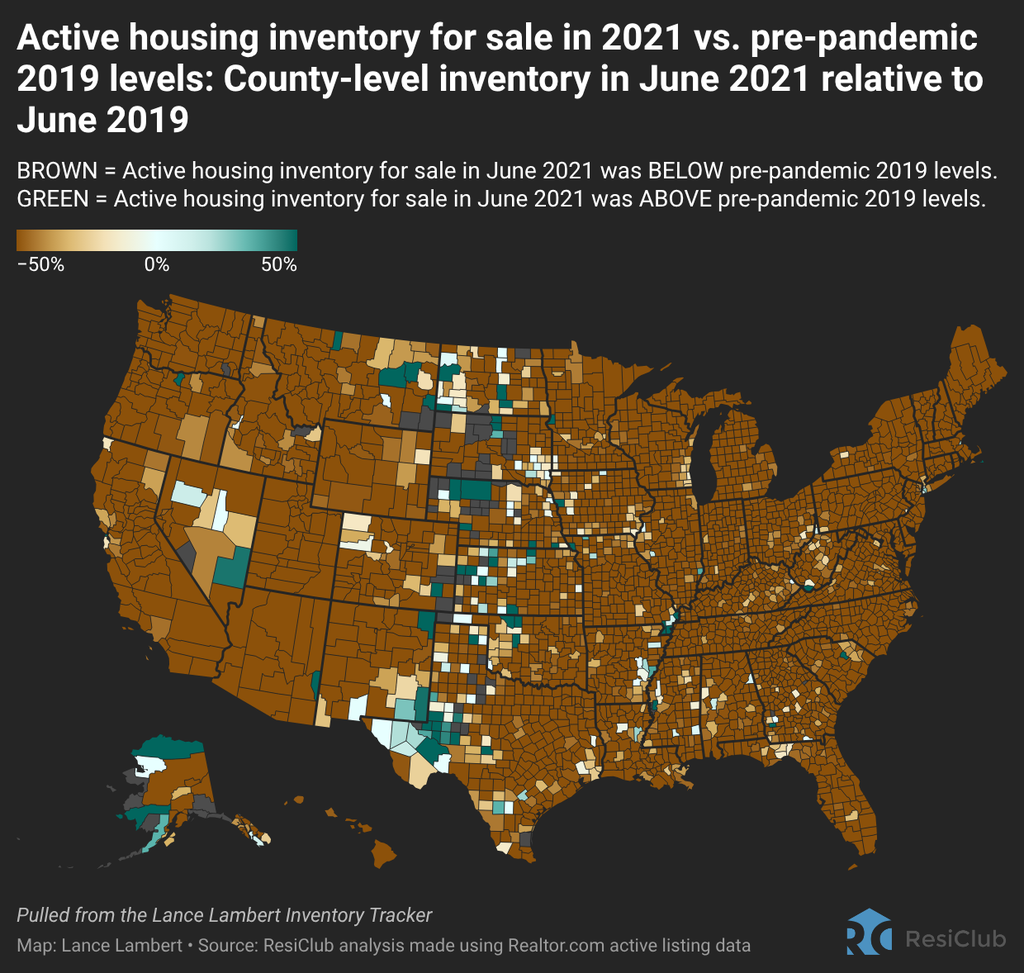

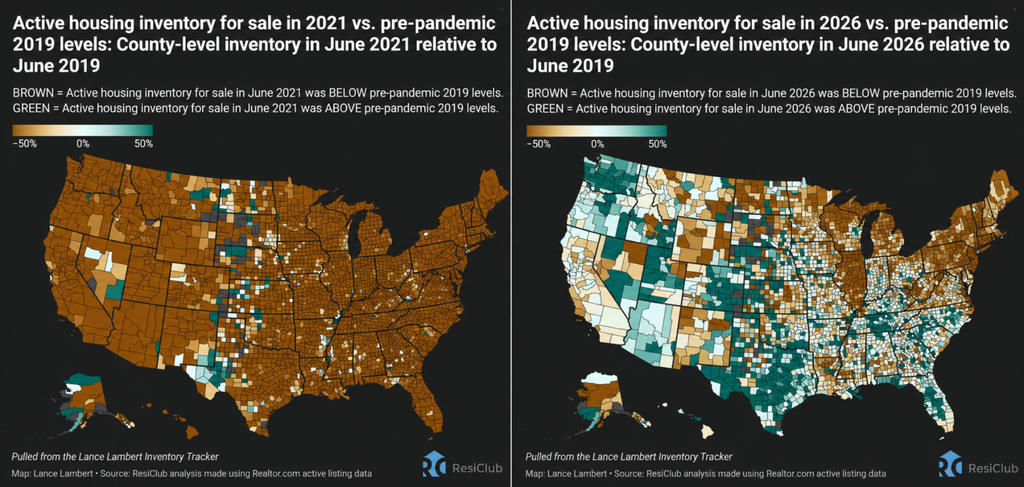

In fact, during the voracious demand for housing at the height of the pandemic housing boom in April 2022, almost the entire country was at least 50% below 2019 pre-pandemic active inventory levels.

Brown = Active inventory of homes for sale in June 2021 was below 2019 pre-pandemic levels

Green = Active inventory of homes for sale in June 2021 was above 2019 pre-pandemic levels

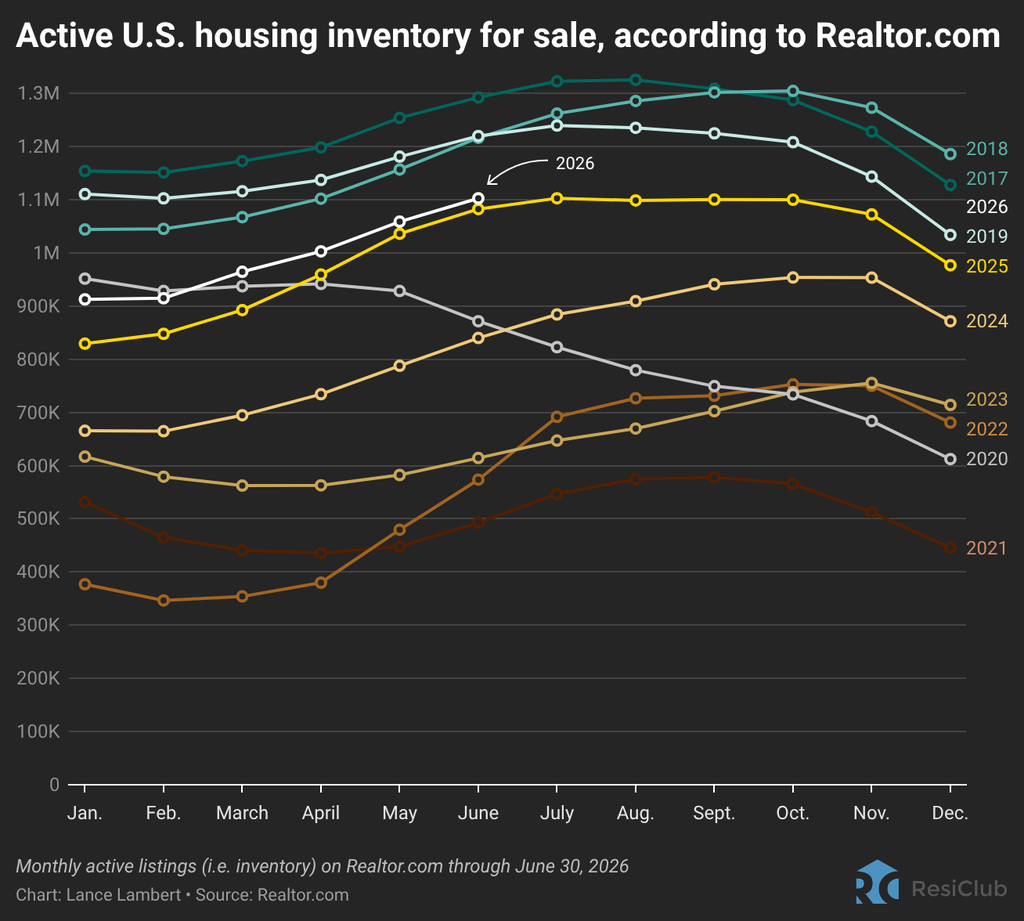

Of course, the picture is different now: national active inventory has been rising for several years (although recently the pace has slowed to a crawl).

Not long after mortgage rates soared in 2022, causing affordability to reflect the reality of sharp home price increases during the pandemic housing boom, and back-to-office mandates gained momentum, national demand in the for-sale market retreated and the pandemic housing boom fizzled out.

Initially, in the second half of 2022, that pullback in housing demand triggered a “rush” in several markets, particularly in the rate-sensitive West Coast housing markets and in pandemic boom cities like Austin and Boise, Idaho, causing active inventory to rise and pushing those markets into a correction mode in the second half of 2022.

Looking ahead to 2023, many of those same pandemic boomtown and Western markets (excluding Austin) stabilized, as seasonal spring demand, coupled with still-tight active inventory levels, was enough to temporarily firm the market. For a time, the national active inventory stopped increasing year after year.

However, this period of stabilization of the national inventory did not last. Amid still sagging housing demand, national active inventory began to rise again and we are now in the midst of a 32-month streak of year-over-year increases in national active listings. (However, domestic inventory growth has recently slowed from +28.9% year-over-year at this time last year to just +1.9% year-over-year between June 2025 and June 2026.)

This period of inventory recovery has coincided with a slowdown in national year-over-year existing home price growth in most indices to around +1.0%. Even as this post-boom period of inventory growth plateaus, it has done enough to get us into a window in which national resale home price growth is now below U.S. income growth (+3.4%), slowly helping to soften the overheating that occurred during the pandemic housing boom.

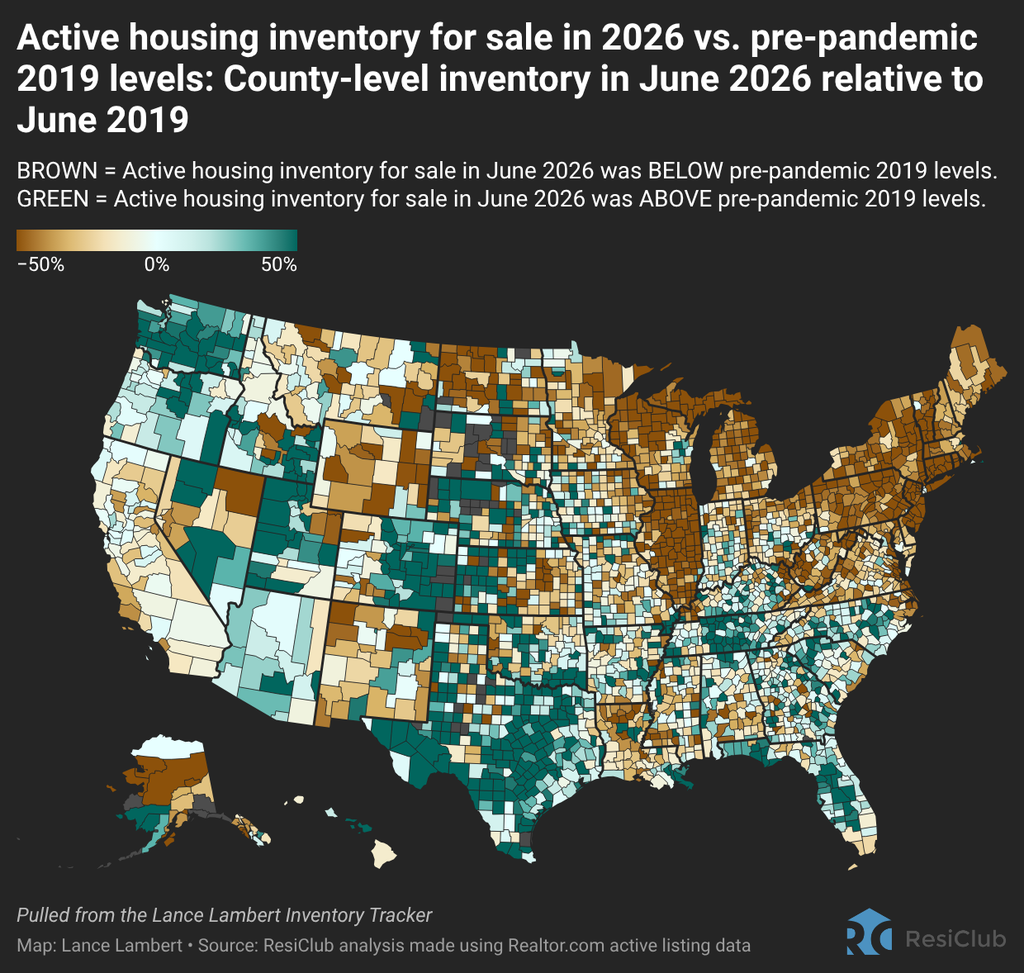

Where active inventory/months of supply has increased the most, homebuyers have gained the most leverage. Generally speaking, housing markets where inventory (i.e., active listings) have returned to pre-pandemic 2019 levels have experienced weaker home price growth (or outright declines) over the past 48 months. In contrast, housing markets where inventory remains well below 2019 pre-pandemic levels have generally experienced stronger home price growth over the past 48 months.

Brown = Active inventory of homes for sale in June 2026 was below 2019 pre-pandemic levels

Green = Active inventory of homes for sale in June 2026 was above 2019 pre-pandemic levels

Click here for an interactive version of the map below.

Ash ResiClub As he has documented in detail, that picture varies significantly across the country: Much of the Northeast and Midwest remain below 2019 pre-pandemic inventory levels, while many parts of the mountainous West and Gulf regions have recovered.

Many of the weakest real estate markets, where homebuyers have gained the most leverage over the past four years, are in the Gulf Coast and Mountain West regions.

These areas were among the country’s biggest pandemic boom cities, and had seen a significant increase in home prices during the pandemic housing boom, which extended housing fundamentals far beyond local income levels. When pandemic-driven internal migration slowed and mortgage rates soared, markets like Cape Coral, Florida, and San Antonio, Texas, faced challenges as they had to rely on local incomes to support strong home prices.

The weakening housing market in these areas was further accelerated by higher levels of new housing supply in the pipeline across the Sunbelt. Builders in these regions are often willing to reduce prices or make other affordability adjustments to maintain sales in a changing environment. These adjustments in the new construction market also create a cooling effect on the resale market, as some buyers who might have opted for an existing home shift their focus toward new homes where offers are still available.

By contrast, many markets in the Northeast and Midwest were less reliant on pandemic migration and had less new home construction underway. With less exposure to that demand shock from retreating internal migration (and fewer builders making large affordability adjustments to move product), active inventory in these Midwest and Northeast regions has remained relatively tight, and home sellers retain more power relative to their peers in the Gulf and Mountain West regions.

While national active inventory at the end of June 2026 was still 9.6% below June 2019 before the pandemic, it is much closer than it was in June 2021, when it was 59.6% below June 2019 before the pandemic.

Big picture: The housing market is still going through a normalization process following a surge in housing demand during the pandemic housing boom, when home prices rose too high, too fast. To date, that normalization process has pushed some markets, including Austin (mid-2022-present), Las Vegas (2nd half of 2022), Phoenix (2nd half of 2022), Boise (mid-2022-2023), Punta Gorda (2022-present), Cape Coral (2023-present), and Tampa, Florida (2024-present), into correction mode. So far, in some other areas, it has caused house price growth to stagnate.

Meanwhile, some markets remain tense and have seen only a slowdown in home price growth from the highs of the pandemic housing boom. As this happens, and national incomes continue to rise (3.4% year over year), underlying fundamentals are slowly improving and softening the overheating that occurred during the pandemic housing boom.